News & Insights

Recent Posts

- Looking for Funding? Consider SBA Loans

- Protect Yourself From Fraudsters Impersonating the IRS and Other Tax Scams

- Self-Employed? Don’t Overlook a Roth IRA

- Knowing What’s Coming: Why Every Local Government Needs a Capital Improvement Plan

- Is an Advisory Board the Right Solution for Your Nonprofit?

- Three Key Considerations for Effective Grant Management in Local Governments

- What You Can Do to Protect Your Business from Rising Costs

- When Outstanding Invoices Indicate Underlying Operational Issues

How to Plan for Succession: Paving the Way for Continued Prosperity

Proficient chess players begin each game with a clear strategy that prepares multiple moves in advance. While each move is designed to set up the next, a strategic chess player will remain adaptable to changing circumstances. This same approach of strategic forethought, flexibility, and responsiveness is best practices for succession planning in wealthy families.

Transitioning Leadership and Management

Succession will happen—it’s a matter of when, not if—so families should prioritize proactive planning to ensure a smooth, successful transition. Unfortunately, data highlights the consequences of inadequate succession planning: Although more than 30% of family-owned businesses transition successfully to the second generation, just 12% of those businesses are viable for the third generation, and a mere 3% are operating by the fourth generation, according to Family Business Review.

There are many aspects to robust succession planning, which, when done well, can help align decision-making and strengthen family unity. The succession plan should address transitioning both the ownership and control of the family wealth enterprise as well as the leadership and management of the family office and, if applicable, the business too.

There are several key factors when transitioning leadership and management, and while the required skill sets will vary depending on the specific roles, the necessary considerations are similar. Diligent and nimble succession planning helps pave the way for continued prosperity in the family wealth enterprise. We’ve identified three different scenarios that encompass most transitions, but the decision-making about succession varies in significant ways across those scenarios.

Central Considerations for Leadership and Management Roles

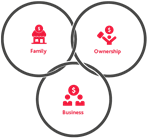

The family wealth enterprise has three interconnected circles of participation—the family members, the family’s business, and the ownership of wealth—and each circle has a distinct lifecycle, but these lifecycles may not always correspond. That’s why having a detailed succession plan is so critical.

There are several key factors to consider when transitioning leadership and management, and while the required skill sets will vary depending on specific roles, the necessary considerations are similar. For example, when planning for succession, the person taking on ownership and leadership roles may be the same individual, but often they are not. Overall, the plan must outline how to assess a candidate’s characteristics in two main areas: interpersonal skills and professional experience.

People Considerations

Whether someone is a family member or not, assuming a leadership role will require the same traits, such as humility, accountability, maturity, integrity, and diligence. The candidates for management or executive positions should possess these characteristics, even if they do not have an ownership role or voting control. A wide range of leadership positions may need to be filled, so the succession plan cannot focus on a single heir. For example, a management role in the family office will require a different skill set than someone on the management team of the family business. Thorough succession planning will account for each leadership opportunity and outline the specific preparations necessary.

Each role that transitions should have a detailed job description that defines the core functions and responsibilities. This description should also draw on input from people in that role, which can help identify the required traits and characterize the ideal candidate. A frank evaluation of all candidates’ capabilities will help to assess and address any gaps. There are even certain tools to measure a person’s innate, instinctive strengths, such as the Kolbe A Index. Ongoing evaluations of the candidate can help keep the transition on track, and these evaluations can also be tied to compensation and reported to the board for approval.

A leadership role in the family office requires an understanding of the family’s history and values and a thorough knowledge of any applicable investments. In addition, the successor will need to have a clear grasp of the family’s risk tolerance and its long-term, multi-generational goals. Crucially, this role also calls for the emotional quotient to manage personalities and balance competing interests within the family.

Professional Considerations

For leadership in the family business, the successor needs to have a comprehensive understanding of the business’s products and/or services and be able to advocate for the organization persuasively. They should also have deep-rooted industry knowledge and experience, which will help them tap the best people to fill roles throughout the business. They will need to combine this knowledge and experience with solid business acumen and the ability to manage people to form and articulate a vision for the future that gains firm-wide buy-in.

As applicable, there are important interfaces between the family office, family business, and the family itself. So, it’s essential to have clear controls, boundaries, and communication protocols in place. In addition, the family should bear in mind the three C’s that form the pillars of effective governance: consensus, communication, and consistency. Strong governance practices help facilitate information sharing as appropriate to achieve alignment and maintain unity.

There are several key factors to consider when transitioning leadership and management, and while the required skill sets will vary depending on specific roles, the necessary considerations are similar. For example, when planning for succession, the person taking on ownership and leadership roles may be the same individual, but often they are not. Overall, the plan must outline how to assess a candidate’s characteristics in two main areas: interpersonal skills and professional experience.

People Considerations

Whether someone is a family member or not, assuming a leadership role will require the same traits, such as humility, accountability, maturity, integrity, and diligence. The candidates for management or executive positions should possess these characteristics, even if they do not have an ownership role or voting control. A wide range of leadership positions may need to be filled, so the succession plan cannot focus on a single heir. For example, a management role in the family office will require a different skill set than someone on the management team of the family business. Thorough succession planning will account for each leadership opportunity and outline the specific preparations necessary.

Each role that transitions should have a detailed job description that defines the core functions and responsibilities. This description should also draw on input from people in that role, which can help identify the required traits and characterize the ideal candidate. A frank evaluation of all candidates’ capabilities will help to assess and address any gaps. There are even certain tools to measure a person’s innate, instinctive strengths, such as the Kolbe A Index. Ongoing evaluations of the candidate can help keep the transition on track, and these evaluations can also be tied to compensation and reported to the board for approval.

A leadership role in the family office requires an understanding of the family’s history and values and a thorough knowledge of any applicable investments. In addition, the successor will need to have a clear grasp of the family’s risk tolerance and its long-term, multi-generational goals. Crucially, this role also calls for the emotional quotient to manage personalities and balance competing interests within the family.

Professional Considerations

For leadership in the family business, the successor needs to have a comprehensive understanding of the business’s products and/or services and be able to advocate for the organization persuasively. They should also have deep-rooted industry knowledge and experience, which will help them tap the best people to fill roles throughout the business. They will need to combine this knowledge and experience with solid business acumen and the ability to manage people to form and articulate a vision for the future that gains firm-wide buy-in.

As applicable, there are important interfaces between the family office, family business, and the family itself. So, it’s essential to have clear controls, boundaries, and communication protocols in place. In addition, the family should bear in mind the three C’s that form the pillars of effective governance: consensus, communication, and consistency. Strong governance practices help facilitate information sharing as appropriate to achieve alignment and maintain unity.

Proactive succession planning can help energize family members and encourage their involvement in the family office and business activities. This deliberate planning can also increase the confidence of non-family executives and management by reassuring them about the stability and future prospects for the business. However, if succession planning is inconsistent or inadequate, that can diminish confidence and can have adverse effects, especially if an unqualified leader is chosen.

Effective succession planning is invaluable, but it can only be accomplished by making thorough preparations and outlining specific steps and key tasks, along with a clear transition timeline. Tying the plan to critical objectives and evaluating the progress and effectiveness of the transition on a recurring basis will help the family business stay on track for continued prosperity.

The Role of Non-family Leadership in the Succession Plan

Even if a family retains full ownership and control of the family wealth enterprise, certain non-family individuals can play a critical role in succession planning. This can include experienced advisors who are involved in the family office, non-family leadership within the business, and other outside experts. Any trusted person who has familiarity with the family and influence with key members can provide helpful input about developing and carrying out the succession plan. In addition, gaining the perspective of someone outside the family can broaden perspective and lend valuable insight to inform consequential decisions.

Three Scenarios for the Succession of Leadership and Management

Families should always be looking to identify and deliberately prepare successors for leadership and management roles among the rising generations. This is a core practice for effective family office governance and risk management. It’s also essential to have a contingency plan in case of the unexpected, such as if the designated heir is unable to fill the role for any reason.

There are three main scenarios for how the succession of leadership and management proceeds, and each one raises distinct questions that must be addressed:

Proactive succession planning can help energize family members and encourage their involvement in the family office and business activities. This deliberate planning can also increase the confidence of non-family executives and management by reassuring them about the stability and future prospects for the business. However, if succession planning is inconsistent or inadequate, that can diminish confidence and can have adverse effects, especially if an unqualified leader is chosen.

Effective succession planning is invaluable, but it can only be accomplished by making thorough preparations and outlining specific steps and key tasks, along with a clear transition timeline. Tying the plan to critical objectives and evaluating the progress and effectiveness of the transition on a recurring basis will help the family business stay on track for continued prosperity.

The Role of Non-family Leadership in the Succession Plan

Even if a family retains full ownership and control of the family wealth enterprise, certain non-family individuals can play a critical role in succession planning. This can include experienced advisors who are involved in the family office, non-family leadership within the business, and other outside experts. Any trusted person who has familiarity with the family and influence with key members can provide helpful input about developing and carrying out the succession plan. In addition, gaining the perspective of someone outside the family can broaden perspective and lend valuable insight to inform consequential decisions.

Three Scenarios for the Succession of Leadership and Management

Families should always be looking to identify and deliberately prepare successors for leadership and management roles among the rising generations. This is a core practice for effective family office governance and risk management. It’s also essential to have a contingency plan in case of the unexpected, such as if the designated heir is unable to fill the role for any reason.

There are three main scenarios for how the succession of leadership and management proceeds, and each one raises distinct questions that must be addressed:

There are several key factors to consider when transitioning leadership and management, and while the required skill sets will vary depending on specific roles, the necessary considerations are similar. For example, when planning for succession, the person taking on ownership and leadership roles may be the same individual, but often they are not. Overall, the plan must outline how to assess a candidate’s characteristics in two main areas: interpersonal skills and professional experience.

People Considerations

Whether someone is a family member or not, assuming a leadership role will require the same traits, such as humility, accountability, maturity, integrity, and diligence. The candidates for management or executive positions should possess these characteristics, even if they do not have an ownership role or voting control. A wide range of leadership positions may need to be filled, so the succession plan cannot focus on a single heir. For example, a management role in the family office will require a different skill set than someone on the management team of the family business. Thorough succession planning will account for each leadership opportunity and outline the specific preparations necessary.

Each role that transitions should have a detailed job description that defines the core functions and responsibilities. This description should also draw on input from people in that role, which can help identify the required traits and characterize the ideal candidate. A frank evaluation of all candidates’ capabilities will help to assess and address any gaps. There are even certain tools to measure a person’s innate, instinctive strengths, such as the Kolbe A Index. Ongoing evaluations of the candidate can help keep the transition on track, and these evaluations can also be tied to compensation and reported to the board for approval.

A leadership role in the family office requires an understanding of the family’s history and values and a thorough knowledge of any applicable investments. In addition, the successor will need to have a clear grasp of the family’s risk tolerance and its long-term, multi-generational goals. Crucially, this role also calls for the emotional quotient to manage personalities and balance competing interests within the family.

Professional Considerations

For leadership in the family business, the successor needs to have a comprehensive understanding of the business’s products and/or services and be able to advocate for the organization persuasively. They should also have deep-rooted industry knowledge and experience, which will help them tap the best people to fill roles throughout the business. They will need to combine this knowledge and experience with solid business acumen and the ability to manage people to form and articulate a vision for the future that gains firm-wide buy-in.

As applicable, there are important interfaces between the family office, family business, and the family itself. So, it’s essential to have clear controls, boundaries, and communication protocols in place. In addition, the family should bear in mind the three C’s that form the pillars of effective governance: consensus, communication, and consistency. Strong governance practices help facilitate information sharing as appropriate to achieve alignment and maintain unity.

Proactive succession planning can help energize family members and encourage their involvement in the family office and business activities. This deliberate planning can also increase the confidence of non-family executives and management by reassuring them about the stability and future prospects for the business. However, if succession planning is inconsistent or inadequate, that can diminish confidence and can have adverse effects, especially if an unqualified leader is chosen.

Effective succession planning is invaluable, but it can only be accomplished by making thorough preparations and outlining specific steps and key tasks, along with a clear transition timeline. Tying the plan to critical objectives and evaluating the progress and effectiveness of the transition on a recurring basis will help the family business stay on track for continued prosperity.

The Role of Non-family Leadership in the Succession Plan

Even if a family retains full ownership and control of the family wealth enterprise, certain non-family individuals can play a critical role in succession planning. This can include experienced advisors who are involved in the family office, non-family leadership within the business, and other outside experts. Any trusted person who has familiarity with the family and influence with key members can provide helpful input about developing and carrying out the succession plan. In addition, gaining the perspective of someone outside the family can broaden perspective and lend valuable insight to inform consequential decisions.

Three Scenarios for the Succession of Leadership and Management

Families should always be looking to identify and deliberately prepare successors for leadership and management roles among the rising generations. This is a core practice for effective family office governance and risk management. It’s also essential to have a contingency plan in case of the unexpected, such as if the designated heir is unable to fill the role for any reason.

There are three main scenarios for how the succession of leadership and management proceeds, and each one raises distinct questions that must be addressed:

- A family member has been identified to take over, and they’ve had thorough preparation along with participation in the family office or business. How can you best set them up for success in terms of planning and communication around the transition?

- A family member has been identified to take over, but they might be too young or don’t have the skills yet. How can you vet them to determine readiness, and what do you do in the interim?

- No family member wants to take over, no one is prepared, or no one is qualified. What is the process to pick a non-family successor or determine the future of the business?

- Family Member: Compensation should be commensurate with the heir’s skills, experience, and performance relative to similar roles at other organizations.

- Non-Family Individual: Compensation should be reviewed closely and subject to board approval.

- Non-public Investors: Compensation can be structured to avoid giving up equity and maintain full ownership

- Set a clear and flexible strategy for transitioning leadership and management roles.

- Have a contingency plan in place should circumstances change.

- Outline directives for family and non-family successors, including personality traits, business acumen, responsibilities, and compensation.

The materials provided in the News & Insights section are for general informational purposes only and may not reflect the most current legal, tax, or financial developments. While we strive to ensure accuracy at the time of publication, Maner Costerisan does not guarantee that the information remains up-to-date or free from error. We recommend consulting directly with a Maner Costerisan team member to confirm the applicability and relevance of any information to your specific situation.